Maritime transport is dominated by shipping line consortia and alliances that are exempt from European competition rules. The EU wants to keep it that way, but its case does not look too strong.

By Olaf Merk

On 20 November, the European Commission released its proposal on the “Consortia Block Exemption Regulation” for shipping lines. What sounds like some obscure bureaucratic rule of little interest managed to upset almost everyone in the maritime logistics chain – from shippers to freight forwarders and the towage sector to port terminal operators. The latter qualified the proposal as “alarming and bewildering” and even threatened court action.

What is the fuss about?

Liner shipping has traditionally been organised in so-called “shipping conferences”, de-facto cartels. Within the European Union, conferences are no longer allowed. But shipping companies can co-operate in the form of consortia, or in bundles of consortia called alliances.

The difference between a cartel and a consortium is that cartel participants collude to improve their profits and dominate the market. Consortia, on the other hand, are tools for co-operation in practical matter, for instance for sharing ship capacity.

The EU’s Consortia Block Exemption Regulation (BER) for liner shipping sets the rules for such co-operation. It exists since 1995 and was revised in 2010. Since then, it has been renewed, without modifications, every five years. The Commission’s proposal that created such a storm is to once more renew the BER without modifications.

Cartels in disguise?

So what caused the backlash now, when in the past the extension of the BER was a mere formality? At the heart of the controversy is the fear that a cartel-like constellation might be re-emerging under the guise of the current regime. For consortia could, in practice, act like cartels if they effectively co-ordinated not just schedules and other practicalities of operation between competitors, but also the price or the available capacity.

And indeed the cost calculation models in the three global shipping alliances allow carriers of the respective alliance “to develop a fine sense of the costs of other carriers”, according to a recent ITF study on liner shipping alliances. And the European Commission raised concerns that carriers might have engaged in price signalling via their announcements of general rate increases.

Joint capacity planning for “adjustments in response to fluctuations in supply and demand” is allowed by the BER. But there is evidence that carriers might have co-ordinated orders for new mega-ships as well as the timing of ship dismantling within alliances.

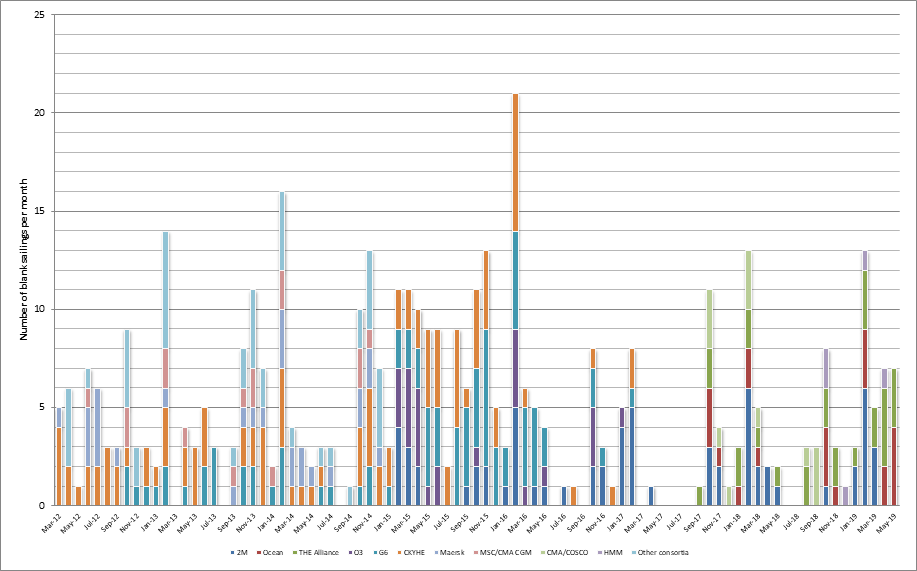

Also, most of the so-called blank sailings – the cancellation of a scheduled weekly service – are done simultaneously by different consortia and alliances, as shown in Figure 1. While some interpret this as joint “capacity adjustments in response to fluctuations in supply and demand”, others might suspect concerted action to influence freight rates. Because the different shipping consortia and alliances are heavily intertwined (Figure 2) even detailed co-ordination between them is not particularly difficult.

Figure 1: Blank sailings per month per alliance (2012-2019)

Figure 2: Overlapping consortia links between carriers (for trades to/from Europe)

Will there really be legal certainty?

For many observers, renewing the BER without modifications in this context raises three major questions. The first relates to legal certainty, which the BER is said provide for carriers. Without the BER, consortia would need to carry out self-assessments to ensure they meet the EU’s general competition regulation.

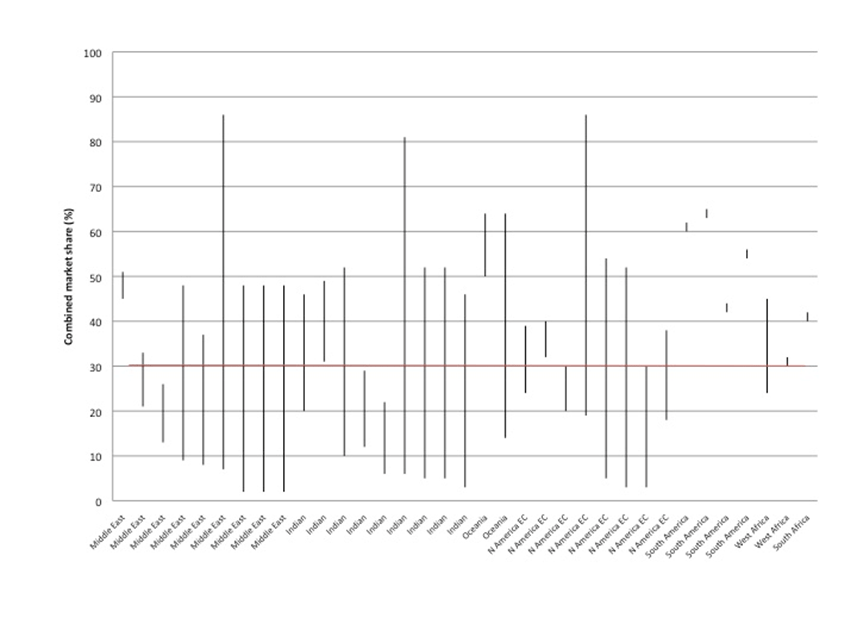

Yet an unmodified BER may not provide this legal certainty, because it is unclear which consortia are still covered by it: it applies only to consortia with a market share below 30%, which is difficult to monitor in practice. The reason is that the Commission uses the “combined market share”, which takes the cross-linkages between consortia into account (illustrated in Figure 2).

That is the right benchmark to look at in principle, but also creates uncertainty as to which consortia fall below and above the ceiling (Figure 3). The Commission recognises that it does not have the data. Collecting it would help to provide legal certainty, but that does not seem to be on the cards.

Other updates would also provide added legal certainty. It is not quite clear whether alliances are still covered by the BER, for instance. And the definition of “relevant markets” no longer reflects the reality of today’s port competition.

Figure 3: Ranges of uncertainty on combined market shares on consortia covering Europe

A matter of market share

The second question is about economic concentration. Consortia were invented as tools to allow smaller shipping lines to achieve scale and compete. Since then, consolidation in the shipping sector has surpassed any previous expectations. The market share of Danish shipping giant Maersk alone was 19% in 2018, larger than the share any alliance had until 2012. So consortia have not been the alternative for market consolidation, they have in fact come on top of consolidation and provided an additional tool for an increasingly consolidated sector to benefit from scale.

The result is that a few alliances have huge buying power and can play off their service providers, such as ports, against each other. For the alliances’ customers the result is reduced choice to transport their goods, because the ocean transport offers are mostly similar.

These aspects are mostly absent from the considerations by the European Commission, which concludes that service quality has remained stable. But the number of direct port-to-port connections has fallen, as have weekly service frequencies. The Commission paper also finds no indications for market power of carriers vis-à-vis ports, yet several examples are documented, including the ports of Malaga, Taranto, Gioia Tauro, Zeebrugge or Genoa.

The politics of liner shipping

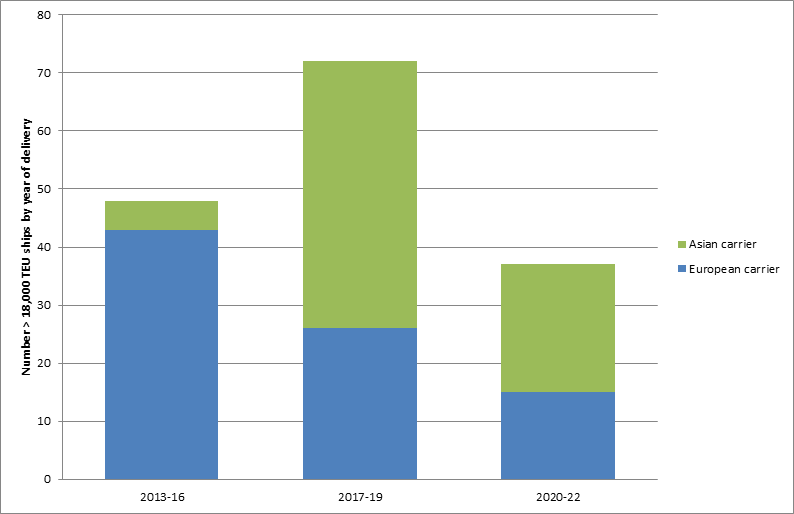

The third question being asked is about the transparency of the process leading to the decision to extend the BER. The Commission’s stakeholder consultation ended in December 2018 but the document was not released until almost a year later, in November 2019. This was only days before a new Commission took office. Some might think the continuation of the BER will protect European liner shipping companies. But in fact the BER has arguably done the opposite, by helping the emergence of Chinese liners. Asian liner companies have ordered large numbers of mega-ships recently (see Figure 4) and to fill that capacity they will need the alliances and consortia more than the Europeans. Interestingly, the Chinese liner company COSCO submitted a document to the European Commission arguing for extending the BER.

Figure 4: Mega-ship deliveries for Asian and European carriers (2013-2022)

The BER might benefit global liner shipping companies, a few of which are headquartered in Europe. It will do less for European shipping companies operating exclusively in Europe, such as feeder companies and tonnage providers (i.e. ship owners who charter out their vessels to liner companies).

Evolution or Big Bang?

The agenda of the new European Commission that took office in December 2019 emphasises industrial policy, geopolitics and a European Green Deal. How the extension of the current BER aligns with these priorities is not so clear. But if it is deemed essential to keep a shipping-specific exemption from EU competition rules, maybe this is the time to re-imagine its conditions.

One could think of a block exemption that only applies to liner companies that pre-dominantly operate in EU waters, or only for consortia on intra-EU routes, or for types of ships (“Europe class” vessels) that meet certain criteria, for instance with regard to energy efficiency, shares of EU seafarers and use of EU-approved ship recycling facilities. Not exactly a Big Bang, but at least some steps that could help implement the agenda of the new Commission, as exemplified by the Green Deal, and give the blanket exemption a new legitimacy that is currently in some doubt.

Olaf Merk is ports and shipping expert at the International Transport Forum. He is the author of Container Shipping in Europe: Data for the Evaluation of the EU Consortia Block Exemption Regulation (ITF, 2019). This article draws on research for this report. It does not necessarily represent the views of ITF members